As a Self-Directed IRA account owner, it is your responsibility to be able to identify and differentiate what fees can be paid by the account owner with personal funds and those that must be paid with funds directly from the IRA account. Understanding the difference between custodial administrative fees and investment related fees is essential to ensuring that you DO NOT commit a prohibited transaction. Conducting any prohibited transaction, even unintentionally, will cause your account to lose its qualified tax-protected IRA status. The below information is meant to help guide you to determine what fees must be paid for by the IRA account, as well as the IRS exemption criteria for fees that can be paid with personal non-qualified funds (i.e., via credit card).

Investment Related Expenses & Fees

Regarding investments directed by your IRA account, the IRS prohibits the use of personal non-qualified funds to pay for expenses and/or fees incurred by the investment asset or the affiliated investment company (if applicable). This would be considered a “self-dealing” transaction, providing personal financial gain to the IRA account owner. All investment related fees must be paid with qualified funds directly from the IRA account.

Examples of Investment Related Services (not an all-inclusive list):

- Precious Metal Investments – Depository Fees must be paid by the IRA.

- Digital Currency Investments – The Digital Currency Account Set-up Fee and Annual Depository Fee must be paid by the IRA.

- Rental Property Investments – Any expense related to the property must be paid by the IRA (i.e., insurance, property taxes, maintenance, management, etc.).

- IRA LLC – The administration costs associated with the IRA LLC must be paid by the IRA LLC or the IRA (i.e., initial filing, annual registration, retitling, etc.).

If there are sufficient funds available in the cash balance of the IRA account, the investment related fees (annual and/or transactional fees) will automatically be deducted from the IRA cash balance, unless informed otherwise.

NOTE: If you would like to “reimburse” your IRA account for the investment related expenses or fees, it will be classified as a contribution. A contribution can be made up to the annual maximum amount (i.e., Roth or Traditional IRA limit of $6,000 for 2021) to replace the amount taken for the fee and will be recorded on your tax documents at the end of the year.

IRS Exemptions

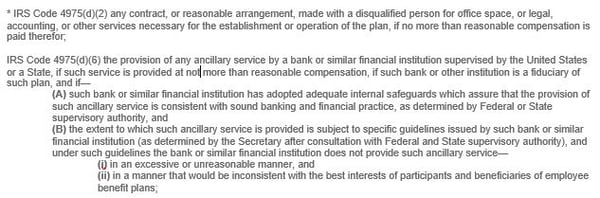

Under the IRS prohibited transaction regulations, fiduciaries and plan service providers fall under the disqualified persons list for “self-dealing” transactions. However, per IRS Code 4975(d)*, there are two exceptions to the prohibited transaction regulations in relation to fees:

- Fees charged for services rendered by the IRA custodian (Preferred Trust Company) that are deemed necessary for the proper establishment and operation of the IRA is NOT considered a prohibited transaction.

- Fees charged for services rendered by legal and/or accounting (CPA) counsel (if applicable) that are deemed necessary for the proper establishment and operation of the IRA is NOT considered a prohibited transaction.

These exemptions are important because it categorizes these fees as administrative, not investment related. This means that the IRA account owner can opt to pay these fees with personal non-qualified funds via credit card (continue reading to learn how).

Custodial Administrative Fees

Administrative fees are incurred for custodial services provided by Preferred Trust Company. As a client, you understand that your IRA account is subject to administrative fees on an annual and transactional basis, dependent on the account value and the investment or account activities directed by you, the IRA account owner. The most up-to-date fee schedule can always be accessed on the Preferred Trust Company website, under the Applications tab by selecting “Fee Schedule”.

Per the IRS exemption mentioned above, the IRA account owner can choose to pay these fees with either the cash (uninvested qualified funds) available within the IRA account or with personal non-qualified funds. Paying these administrative fees with personal funds provides account owners with the opportunity to preserve their IRA funds for new investments or potential investment related expenses.

Examples of Administrative Related Services (not an all-inclusive list):

- Annual Administration Fee

- Real Estate Asset Transaction Fee

- Real Estate Asset Administration Fee

- Trust Deed Investment Transaction Fee

- Digital Currency Transaction Fee

- Precious Metal IRA Account Administration Fee

- Precious Metal Transaction Fee

- Expedited Processing Fee

- Partial Transfer Out Fee

- Cashier’s Check Fee

- Incoming/Outgoing Wire Fee

- IRA Account Conversion Fee

How to Prepay or Reimburse Administrative Fees (ONLY):

If there are sufficient funds available in the cash balance of the IRA account, the administrative fees (annual and/or transactional fees) will automatically be deducted from the IRA cash balance unless otherwise instructed by the IRA account owner. The client has two options to reimburse their account:

- Online Payments: Clients can pay fees 24/7 via credit card online on the Preferred Trust Company client account portal. Login to your account portal, select Accounts and on the right side under "Links" you will select Online Payments. If there are multiple fees that need to be paid, select and add the different fees to your “shopping cart”, review your cart to ensure that everything is correct and then complete the payment with a credit card. Please ensure that you enter your account information correctly so that the payment is applied to the correct account.

- Submit a Credit Card Authorization Form: Credit Card Authorization forms can be submitted via ESign on your account portal or you can download, print and sign the form and return via email to info@ptcemail.com. If there is already a Credit Card Authorization form on file with Preferred Trust Company, you can direct the reimbursement on the card in writing via email to info@ptcemail.com, a phone call will not be accepted.

- To Prepay the annual administrative fee, you must give written notice directing Preferred Trust Company to use the card on file at the beginning of the month that your fee will be taken. Annual administration fees are taken the month prior to the account being opened. For example, if the IRA account was opened in September, then the fee will be taken annually at the end of August.

- To Prepay transactional administrative fees, you must give written notice directing Preferred Trust Company to use the card on file in-advance of the fee being charged.

- Mail a Check: You can send a check by mail. We strongly encourage you to utilize one of the above methods to protect your bank account information from potential fraud if the check were to fall into the wrong hands. If you must send a check by mail, certified mail is recommended.

NOTE: If there are insufficient funds available in the cash balance of the IRA Account but there is a Credit Card Authorization form on file, then Preferred Trust Company will charge the card for the outstanding fees.

Investment and Administrative Fee Reconciliation

Per the Custodial Agreement that you signed in your IRA application (Article VIII, Section 12):

- Preferred Trust Company has the right to liquidate assets in your IRA if necessary to make distributions or to pay fees, expenses, indemnities, taxes, federal tax levies, penalties, or surrender charges properly chargeable against your IRA. If you fail to direct Preferred Trust Company as to which assets to liquidate, we will decide, at our sole discretion, and you agreed not to hold us liable for any adverse consequences that result from our decision.

- In the event that you fail to pay any fees, costs, indemnities, penalties, expenses or payments due to the custodian on-time with personal non-qualified funds or IRA funds (depending on the type of transaction), and there is not a sufficient amount of cash available in the IRA to recoup the total amount due, you will receive a notice and a 10-day grace period to cure the outstanding amount. If the amount remains unpaid past the grace period, the custodian has the right to liquidate assets within the IRA in order to reconcile the amount that is owed.

To learn more about IRS rules and regulations regarding prohibited transactions in a Self-Directed IRA, Click Here.