The IRS just announced that retirement plan contribution limits increased for tax year 2023. Significant adjustments were also made to the income eligibility ranges for retirement plan tax-deductions and Roth IRA contributions.

What is the IRA contribution limits for 2023?

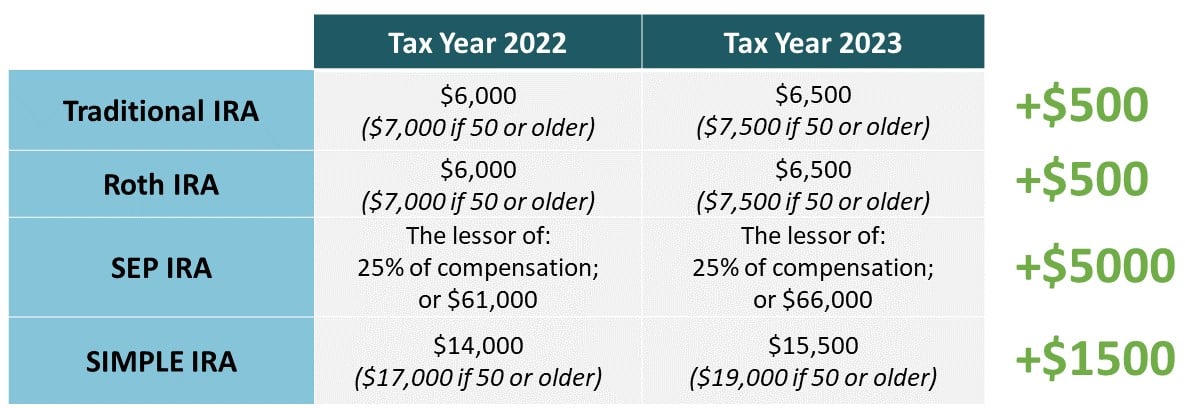

To see what impact the contribution limit increase will have on your IRA account(s), take a look at the chart below

Employer 401k, 403b, most 457 plans, and the federal governments Thrift Savings Plan contribution limits also increased from $20,500 in 2022, to $22,500 for 2023.

Are you eligible for IRA contribution tax-deductions in 2023?

If you or your spouse are covered by an employer retirement plan, certain conditions must be met to deduct contributions to a tax-deferred IRA account (i.e., Traditional, SEP, SIMPLE) from your annual tax burden. The filing status and income of you and/or your spouse effects whether the deduction is “phased-out” (reduced) or eliminated.

The IRS increased eligibility by bumping up the income range criteria that begins to phase-out or eliminate taxpayers from tax-deferred IRA benefits. The following income ranges will go into effect in 2023:

- For single taxpayers, the income range increased to between $73,000 and $83,000 (previously $68,000 and $78,000).

- For married couples filing jointly, if the spouse making the IRA contribution is covered by a workplace retirement plan, the income range is increased to between $116,000 and $136,000 (previously $109,000 and $129,000).

- For an employee who is not covered by a workplace retirement plan and is married to someone who is covered, the income range is increased to between $218,000 and $228,000 (previously $204,000 and $214,000).

- For a married individual filing a separate return who is covered by a workplace retirement plan, the income range is not subject to an annual cost-of-living adjustment and remains between $0 and $10,000.

If neither you nor your spouse is covered by an employer retirement plan, then the income phase-outs do not apply. To learn more about how these changes will affect your household’s deduction eligibility, please consult a tax professional for assistance.

Are you eligible for Roth IRA contributions in 2023?

The filing status and income of you and/or your spouse effects whether the ability to make Roth IRA contributions is phased-out or eliminated. This update does not affect your ability to perform Roth conversions from a tax-deferred retirement account.

To adjust for inflation, the IRS increased eligibility by bumping up the income range criteria that begins to phase-out or eliminate taxpayers from making Roth IRA contributions. The following income ranges will go into effect in 2023:

- For single taxpayers and heads of household, the income range increased to between $138,000 and $153,000 (previously $129,000 and $144,000).

- For married couples filing jointly, the income range increased to between $218,000 and $228,000 (previously $204,000 and $214,000).

- For a married individual filing a separate return who makes contributions to a Roth IRA is not subject to an annual cost-of-living adjustment and remains between $0 and $10,000

To learn more about how these changes will affect your household’s Roth IRA contribution eligibility, please consult a tax professional for assistance.

For more details on these and other retirement-related cost-of-living adjustments for 2023, please review IRS Notice 2022-55.